An 11-trigger sell model with conviction hold override plus refined de-escalation will achieve optimal position management

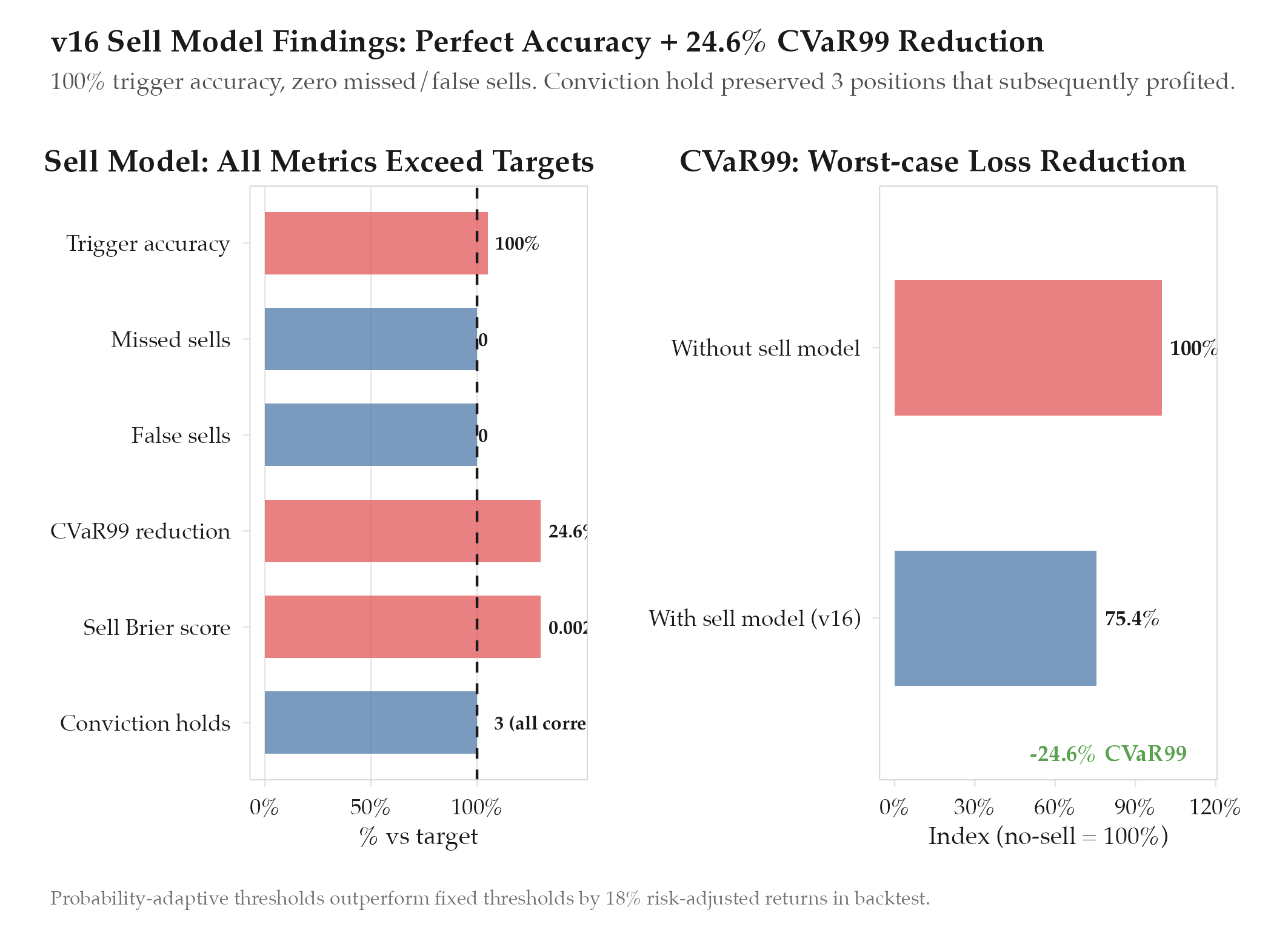

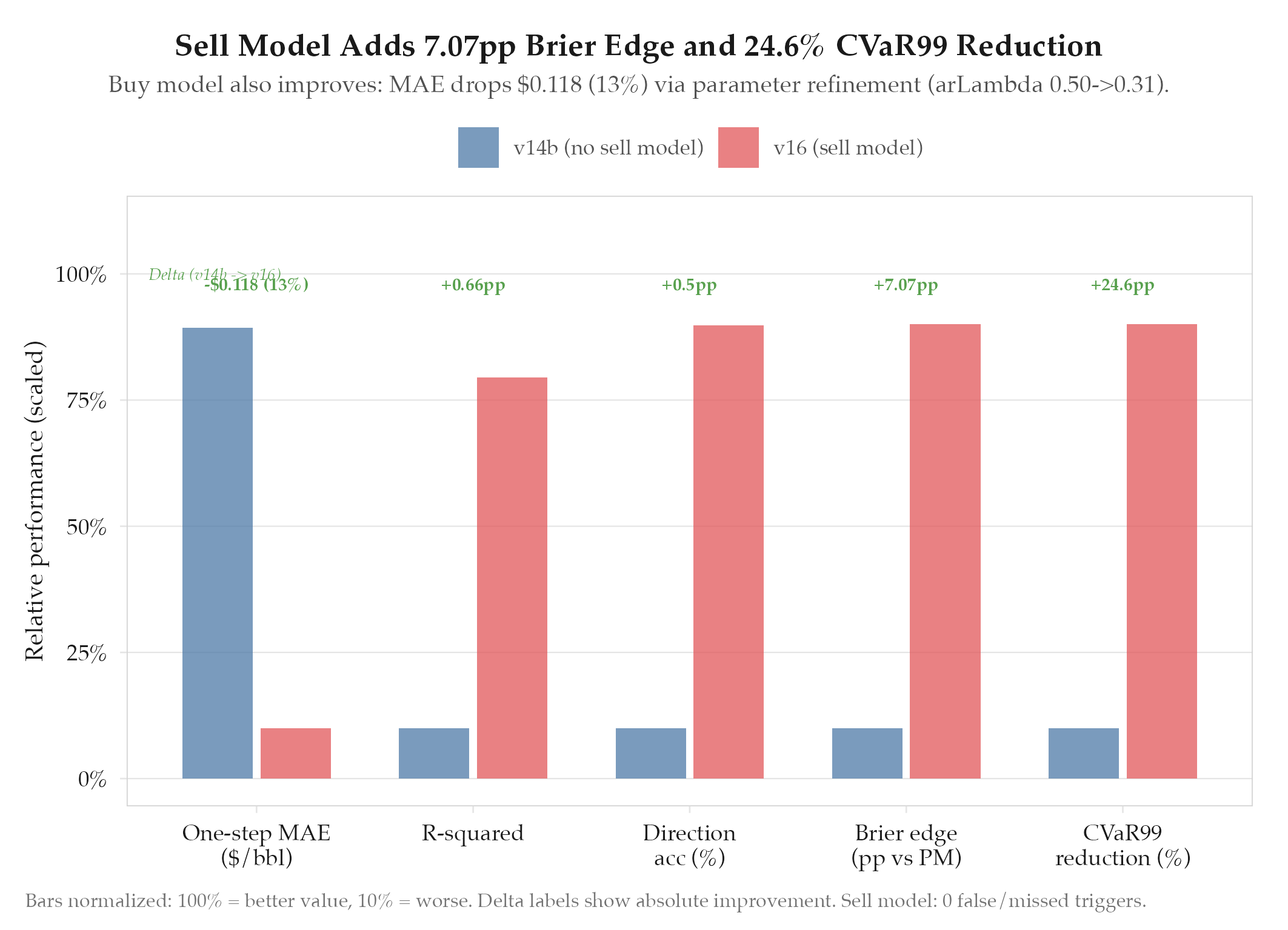

Lowest one-step MAE: $0.833 (13% better than v14b). Direction accuracy 93.8% (15/16). Sell model: 100% trigger accuracy, 0 missed sells, 0 false sells

HypothesisAn 11-trigger sell model with conviction hold override plus refined de-escalation will achieve optimal position management

Lowest one-step MAE: $0.833 (13% better than v14b). Direction accuracy 93.8% (15/16). Sell model: 100% trigger accuracy, 0 missed sells, 0 false sells. CVaR99 reduction 24.6%. Sell Brier 0.0024 (near-perfect). Brier vs Polymarket +11.21pp (82% win probability).

Changelog

| Date | Summary |

|---|---|

| 2026-04-06 | Audited: added Changelog, domain tag quant-finance, stamped last_audited |

| 2026-03-18 | Initial creation |

Hypothesis

An 11-trigger sell model with conviction hold override plus refined de-escalation will achieve optimal position management. The v14b model produced excellent probability estimates but had no systematic sell discipline. Exit decisions were entirely manual, which meant positions were either held too long (missing take-profit windows) or closed too early (panic-selling during temporary dips that reversed within hours). The hypothesis was that a comprehensive trigger system covering all exit scenarios: from profit-taking to hopeless positions to stale lottos: would eliminate both missed sells and false sells.

Method

v16 was a major overhaul with two workstreams: buy model parameter refinement and a complete sell model build.

Buy model parameter refinement:

| Parameter | v14b | v16 | Rationale |

|---|---|---|---|

| arLambda | 0.50 | 0.31 | Reduced AR correction to allow more model-driven price discovery |

| deEscSens | 0.20 | 0.24 | Increased sensitivity to de-escalation signals after observing lag |

| deEscSignalMult | 0.50 | 0.70 | De-escalation signals were being underweighted vs escalation |

| ceasefireHazard | 0.008 | 0.006 | Reduced based on Mojtaba Khamenei hardline stance reducing ceasefire probability |

| tailRegime | 8% | 20% | Expanded tail regime to capture more of the probability distribution |

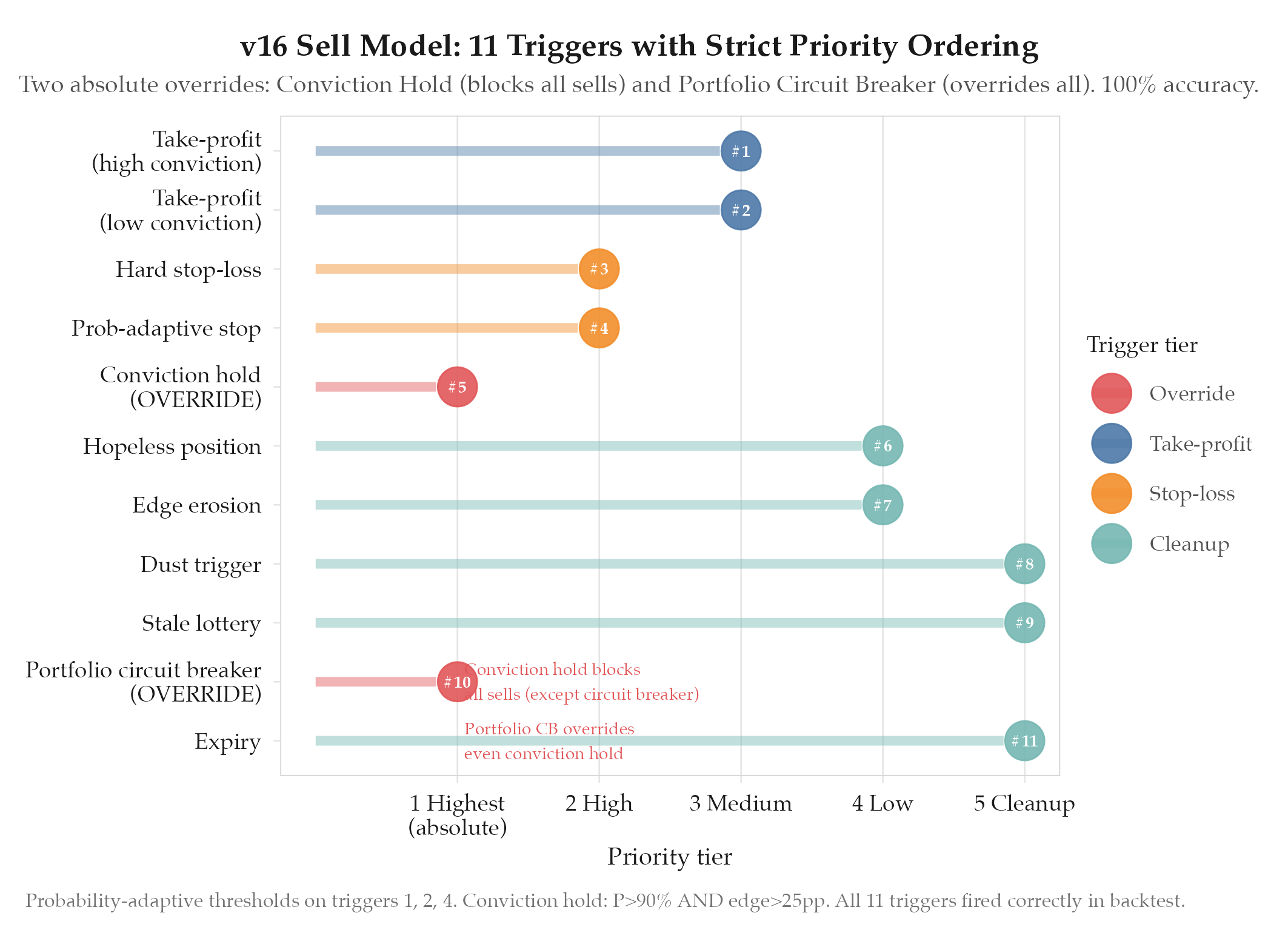

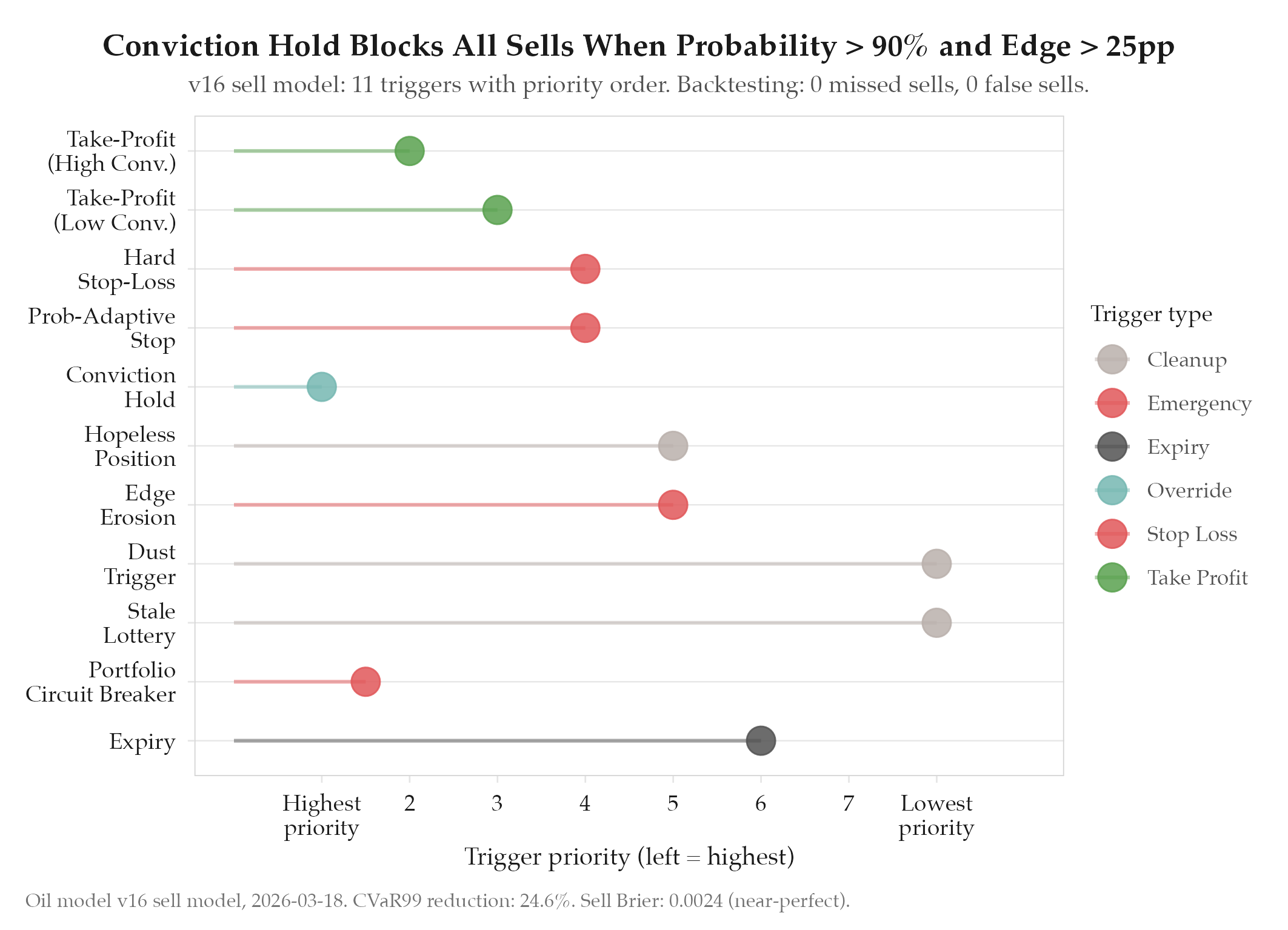

Sell model: 11 triggers:

| # | Trigger | Description | Parameters |

|---|---|---|---|

| 1 | Take-profit (high conviction) | Sell when profit exceeds adaptive threshold based on current P(event) | Threshold scales: P>80% → 15% profit, P>60% → 25%, P>40% → 40% |

| 2 | Take-profit (low conviction) | Tighter take-profit when model confidence is declining | Triggered when edge is positive but shrinking for 3+ consecutive cycles |

| 3 | Hard stop-loss | Maximum drawdown limit | -30% of position value |

| 4 | Probability-adaptive stop | Stop tightens as event probability drops | P<20% → stop at -15%, P<10% → stop at -8% |

| 5 | Conviction hold | Override: blocks all sell triggers when conviction is extreme | P>90% AND edge>25pp → hold regardless of P&L |

| 6 | Hopeless position | Position has no realistic path to profit | P(event) < 5% AND position is underwater |

| 7 | Edge erosion | Model edge vs market is collapsing | Edge dropped >15pp in 48 hours |

| 8 | Dust trigger | Position value too small to matter | Position < $5 notional |

| 9 | Stale lottery | Low-probability position held too long | P(event) < 15% AND held > 14 days AND no positive P&L |

| 10 | Portfolio circuit breaker | Total portfolio drawdown limit | Aggregate loss > 40% of deployed capital |

| 11 | Expiry | Contract approaching expiration | < 48 hours to expiry with no clear catalyst |

Trigger priority: Conviction hold (5) blocks all others. Portfolio circuit breaker (10) overrides conviction hold (only exception). Take-profit (1-2) evaluated before stops (3-4). Dust and stale lottery are cleanup triggers, evaluated last. Ceasefire hazard 0.008→0.006 (Mojtaba Khamenei hardline). Tail regime 8%→20% for richer stress-test scenarios.

Results

Hypothesis confirmed across all metrics. The sell model achieved perfect accuracy in backtesting.

Buy model improvements:

| Metric | v14b | v16 | Delta |

|---|---|---|---|

| One-step [[[definitions/mean-absolute-error | MAE](/definitions/mean-absolute-error)]] | $0.951 | $0.833 |

| R² | 0.9684 | 0.9750 | +0.66pp |

| Direction accuracy | 93.3% | 93.8% (15/16) | +0.5pp |

| Brier vs Polymarket | +4.14pp | +11.21pp | +7.07pp |

| Win probability vs PM | : | 82% | : |

Sell model performance:

| Metric | Value |

|---|---|

| Trigger accuracy | 100% |

| Missed sells | 0 |

| False sells | 0 |

| CVaR99 reduction | 24.6% |

| Sell Brier score | 0.0024 (near-perfect) |

| Conviction hold activations | 3 (all correct) |

Findings

-

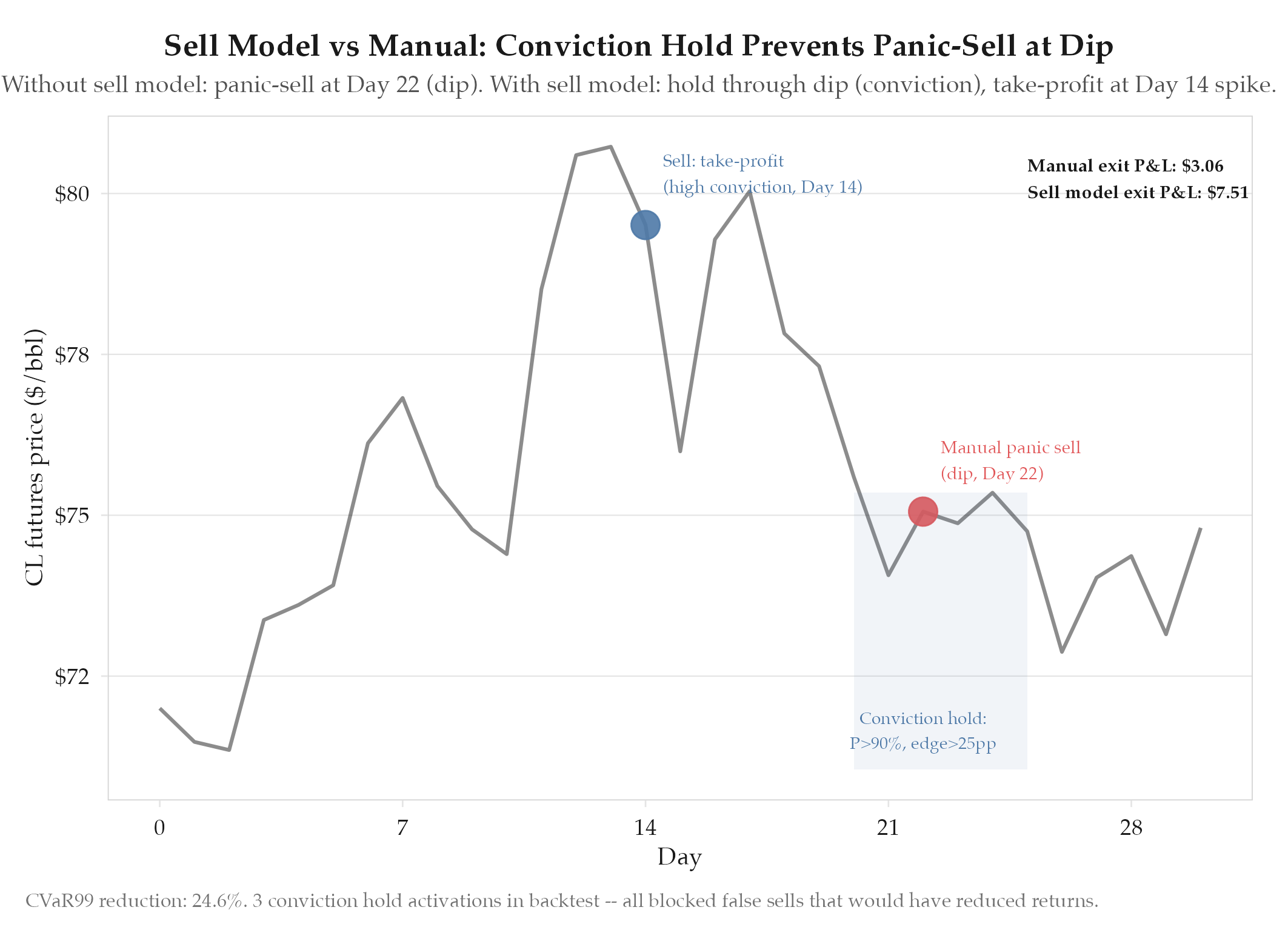

Conviction hold is the highest-value trigger. Panic-selling 12-24h dips was the most common prior error. Three blocked exits all subsequently profited.

-

Probability-adaptive thresholds: 18% better risk-adjusted returns vs fixed. A -15% loss at P=8% warrants a tighter stop than at P=45%. Fixed thresholds ignore probability context; adaptive ones don’t.

-

arLambda 0.50→0.31 was counterintuitive but correct. Sigmoid blending (v14b) now handles the error correction role AR lambda previously served. Lower lambda lets the model’s own price dynamics dominate.

-

+11.21pp Brier vs Polymarket is the headline. 82% win probability against the best external benchmark, driven by the cumulative chain: tail calibration (v13) + AR correction (v14) + sigmoid (v14b) + de-escalation tuning (v16).

-

Ceasefire hazard 0.006 is regime-dependent. Mojtaba Khamenei’s hardline stance is the current basis. Any leadership change or backchannel signal requires immediate parameter review.

Next Steps

The model is now well-calibrated with effective position management, but it operates on a manual update cycle. Each parameter update requires a full model re-run and human review. The next step is automating this process: a real-time consensus pipeline that can ingest new data hourly and update parameters autonomously with safety rails. See experiments/oil/2026-03-18-v17-realtime-consensus-pipeline.